Skip to content

Skip to content

Stealth’ increases

The personal allowance and basic rate band threshold are still frozen at their 2021/22 levels and, subject to the outcome of the next general election, are expected to remain at such until 5 April 2028. As earnings increase, individuals will move into higher tax bands. This is often referred to as ‘fiscal drag’ because it will raise more tax without the government increasing income tax rates.

The tax-free personal allowance of £12,570 continues to be partially and then fully withdrawn for higher earners, with £1 of personal allowance lost for every £2 of adjusted net income over £100,000.

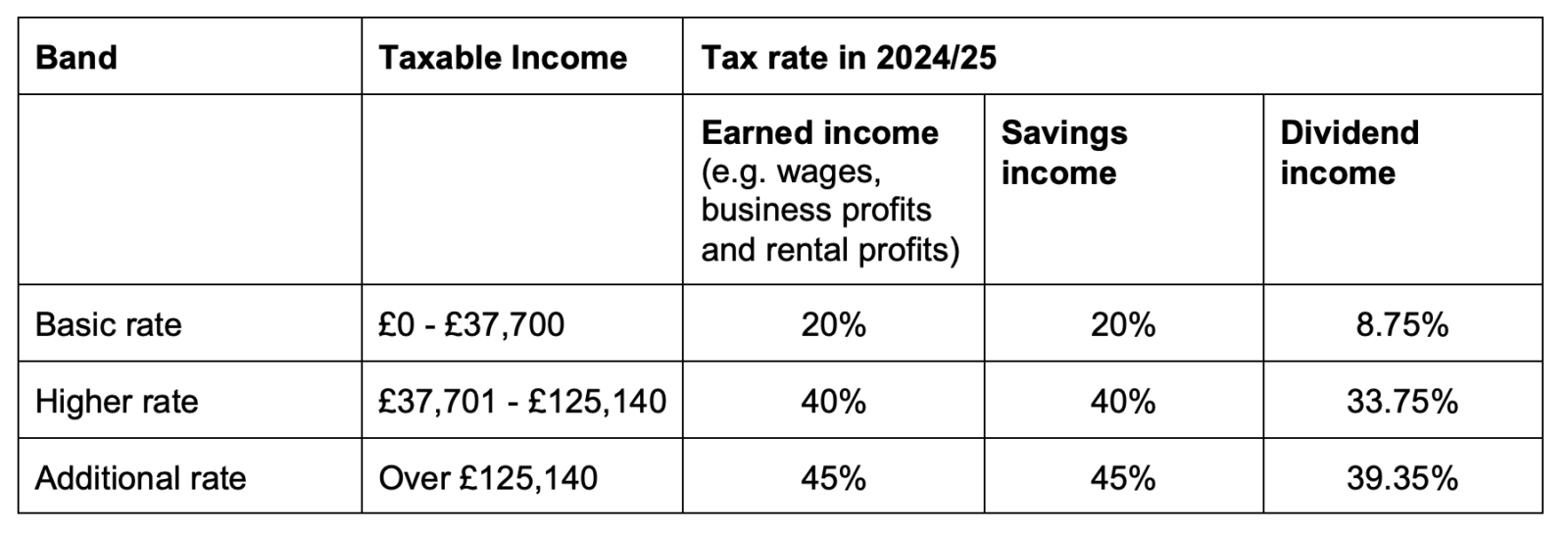

Income tax rates and allowances for 2024/25

Held at their 2023/24 levels, the following income tax rates will apply to taxable income, after the personal allowance has been utilised.

Other allowances

Savings income continues to benefit from a 0% personal savings allowance of £1,000 for basic rate taxpayers and £500 for higher rate taxpayers.

Dividend income attracts a 0% dividend allowance of £500 in 2024/25, down from the £1,000 allowance seen in 2023/24.

Scotland

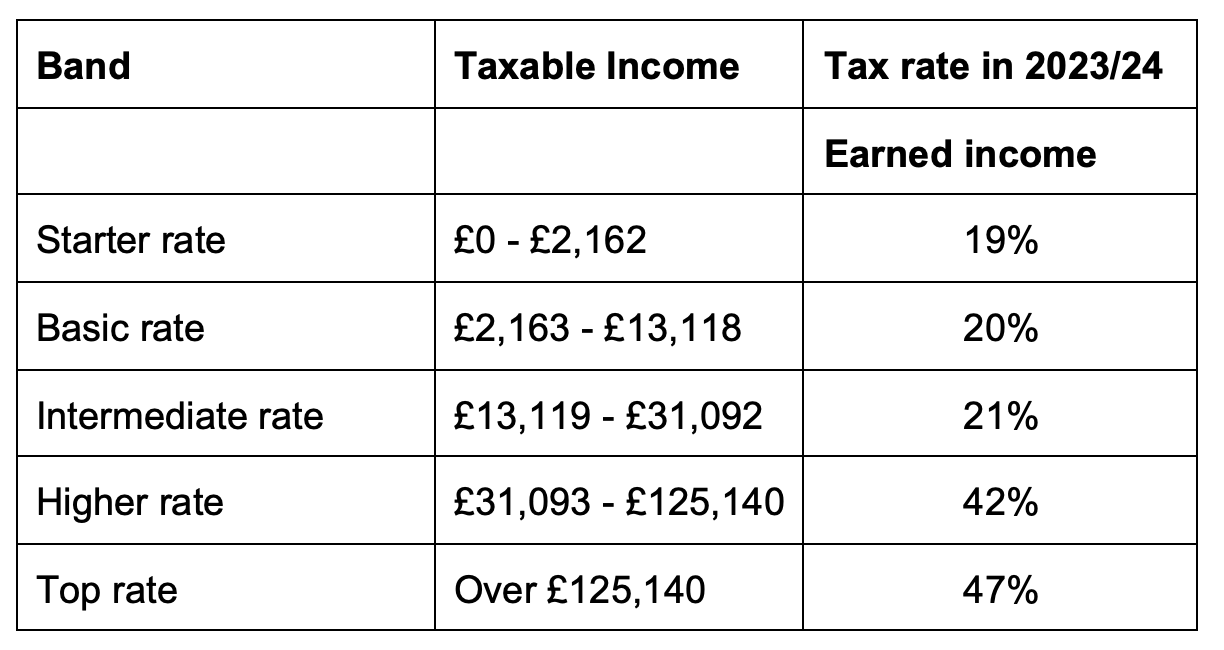

Individuals living in Scotland and classed as Scottish taxpayers are also entitled to the personal allowance of up to £12,570 but have a slightly different banding system for ‘earned income’ as follows:

The application of income tax to savings and dividends income is the same as for taxpayers based elsewhere in the UK.

The Scottish Budget, in which rates and bands for 2024/25 are expected to be announced, is set to take place on 19 December 2023.

Tax Efficient Savings

The annual limits for Individual Savings Accounts (ISAs), Child Trust Funds and the Junior ISA remain at £20,000, £9,000 and £9,000 respectively in 2024/25. The lifetime ISA annual subscription limit also remains unchanged at £4,000 (excluding the government top-up bonus).

The government is making changes to simplify ISAs and provide more choice, meaning it will be easier to choose the best ISA accounts and move money between them. This involves digitalising the ISA reporting system to make it more effective, as well as expanding the investment opportunities available in ISAs.

Pension tax relief

Annual allowances determine the maximum amount that an individual can save into their pension pots in a tax year before tax relief starts to be withdrawn by way of pension tax charges.

These allowances will remain fixed in 2024/25 at their 2023/24 rates, being the £60,000 annual allowance applicable in most circumstances and the £10,000 money purchase annual allowance for those who have flexibly accessed their pension pot. The annual allowance is reduced for those with a high income of more than £260,000.